Scheduled depreciation – deduction for wear and tear, depreciation

Scheduled depreciation shows the “depreciation” and thus the wear and tear of an asset in accounting. They distribute the acquisition or production costs of the fixed assets over the years of use. This means that depreciation is an expense that reduces a company’s profit and is regulated by law in the Commercial Code (HGB) from Section 253.

A brief example of scheduled depreciation

On January 1st, 2016, a company bought a copier for EUR 10,000 net ( acquisition cost ). This device has a typical useful life of 5 years. The depreciation plan distributes the “depreciation”, wear and tear through scheduled depreciation on a straight-line basis over the fiscal years of use. For 2016 to 2020 this means an annual profit-reducing depreciation of 2,000 euros.

In tax law (EStG), depreciation is referred to as depreciation for wear and tear (AfA for short).

The imputed and commercial depreciation

A distinction is often made in companies between imputed and commercial (accounting) depreciation. The imputed depreciation is carried out for the company’s internal calculation and this does not appear in the bookkeeping. Imputed depreciation is only used for cost analysis and cost accounting .

According to polyhobbies, the depreciation under commercial law is the depreciation that is stipulated by the legislator and which must be shown accordingly in the annual financial statements. The fixed depreciations may differ from these depreciations. The replacement values of an asset are often used as the basis for depreciation for imputed depreciation. This is different with commercial depreciation, where the acquisition value or production cost of an asset is applied. This is then amortized over a theoretical useful life. This useful life can be found in the depreciation tables .

What are the scheduled depreciation?

A basic distinction is made between the following scheduled depreciation. These are also called depreciation methods:

- The straight-line depreciation – the standard depreciation

- The declining balance depreciation

- The performance-based depreciation

- The digital depreciation

There is also unscheduled depreciation , which results from the lowest value principle. This means that only the lowest realistic value may be used for such a depreciation.

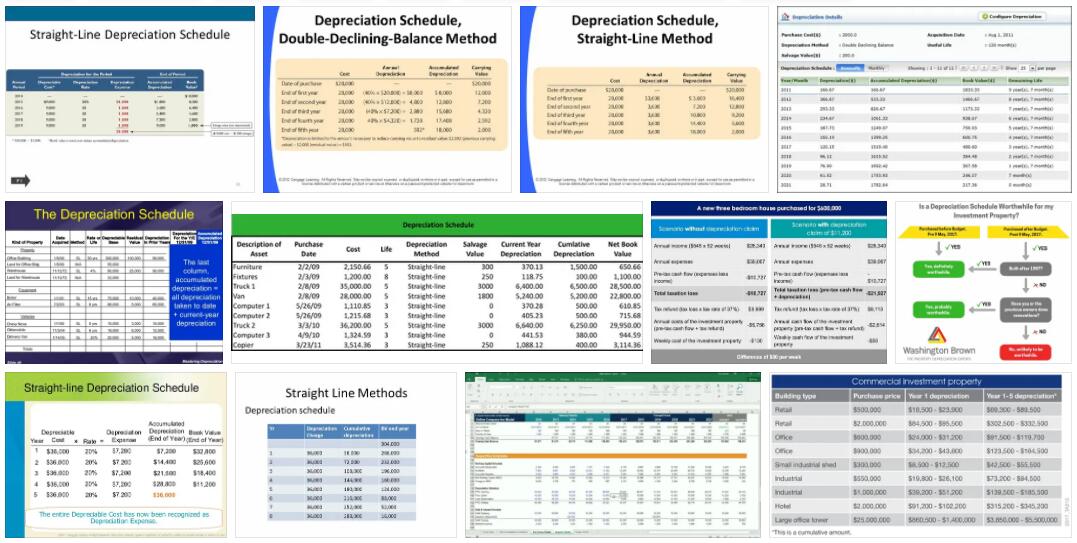

The straight-line depreciation

This is clearly defined by the HGB. Here it is precisely stipulated that economic costs with the corresponding acquisition costs or production costs are to be written off by the company over the planned useful life. Due to the constant amounts that are depreciated annually, there is a linearity and this is where the name “straight-line depreciation” comes from. How high the annual depreciation amount is is calculated from the acquisition or production costs divided by the useful life.

The declining balance depreciation

This is calculated on the basis of a constant depreciation rate, which up to December 31, 2012 was only allowed to be a maximum of 30%. As far as the calculation is concerned, this is done using the residual book value of the asset. Due to the constant depreciation rate, the depreciation amounts decrease over the useful life of the asset and since this calculation never reaches the amount zero, the remaining amount is depreciated as final depreciation in the last year of use.

The declining balance depreciation has been discontinued since January 1st, 2008 by the Corporate Tax Reform Act 2008. This means that only straight-line or performance-based depreciation can be used for all goods purchased in 2008.

The performance-based depreciation

For all assets that were bought up to December 21, 2007, this means that it is possible to use the degressive as well as the straight-line depreciation or the performance-based depreciation. With the emergence of the economic crisis, the declining balance depreciation was temporarily reintroduced by tax law and thus it is possible to depreciate assets between December 21, 2008 and January 1, 2011, but only with 2.5 times the depreciation rate of the linear depreciation and one maximum depreciation rate of 25% for the declining balance depreciation.

The performance-based depreciation can also be used for all assets whose performance or annual use can be proven or measured. This is why this form of depreciation is often used for company vehicles or special machines. But the overall performance of the asset must be known or calculable. The depreciation rate is then calculated from the proportionate performance of the asset to the total output and this proportion is then depreciated from the acquisition or production costs.

The digital depreciation

The digital depreciation is a variant of the arithmetic-degressive depreciation. Here, too, high depreciations are initially carried out over time, which reduce the value of the fixed assets more than later over time.

The depreciation rates for digital depreciation are calculated as follows:

Formula for calculating digital depreciation

The following applies:

AB = depreciation basis = acquisition costs +

incidental acquisition costs – residual value a_T = depreciation amount in the last period of the depreciation period

d = annual reduction in the depreciation amount

T = period

t = period

Write-off on accounts receivable

However, not only fixed assets can be written off in a balance sheet, but also current assets. During this process, write-offs for receivables (also called write-offs on receivables) can occur.

The most common reasons for receivables write-offs are bankruptcies or the unwillingness of customers to pay. The moment a doubt arises as to whether the claim can be collected, it must be reassessed. In practice, such a bad debt is “parked” on a special account in the company’s own bookkeeping. This is generally called “Doubtful Claims”. However, this account is not shown on the balance sheet. Receivables posted there are only written off in the balance sheet when they actually fail.

How can you write off a claim?

- The individual value adjustment, here a single non-collectible claim is corrected.

- The general bad debt allowance, where a flat percentage is written off on all accounts receivable. The percentage is calculated from past experience.

- A mixture of the two methods. Here, the specific receivable is adjusted individually first and then the remaining value adjusted as a lump sum. This method is the most widely used in companies.

Due to the deterioration in payment behavior of debtors in recent years, write-offs on receivables have become more and more important in the past. They are moving more and more into the focus of specialized service providers. So-called ” factoring ” can make write-offs on receivables superfluous, because with this type of service you sell receivables to the factoring provider at a discount. This also reduces the taxable profit, but prevents receivables from failing completely. A write-off on receivables is then hardly necessary.

How is a depreciation rate determined?

Regardless of what you want to write off, the depreciation rate for scheduled depreciation is usually always the same.

A practical example:

- Acquisition cost of a car = 24,000 euros net

- The expected useful life is 6 years.

With straight-line depreciation, the purchase price is divided by the useful life of the asset. This results in the simple calculation: 24,000 euros / 6 years = 4000 euros per year.